WFP Income Fund

Stable Income & Principal Protection®Through Short-Term Fixed Income Investments

WFP Income Fund

The WFP Income Fund (the "Income Fund") is a real estate-based private credit fund designed as a short term fixed income alternative investment that seeks to provide attractive risk-adjusted returns to its investors primarily through the Income Fund’s investments in first trust deeds and mortgages.

We manage a diverse portfolio of loans secured by first liens against real property in the seniors housing, healthcare real estate, multifamily, and commercial real estate sectors around the country. Our investment strategy uses the priority lien position of first loans and targets a conservative loan-to-value ratio to minimize risk, while generating stable income through borrower interest payments made to the fund.

2026 Earnings Call

Stable Net Asset Value

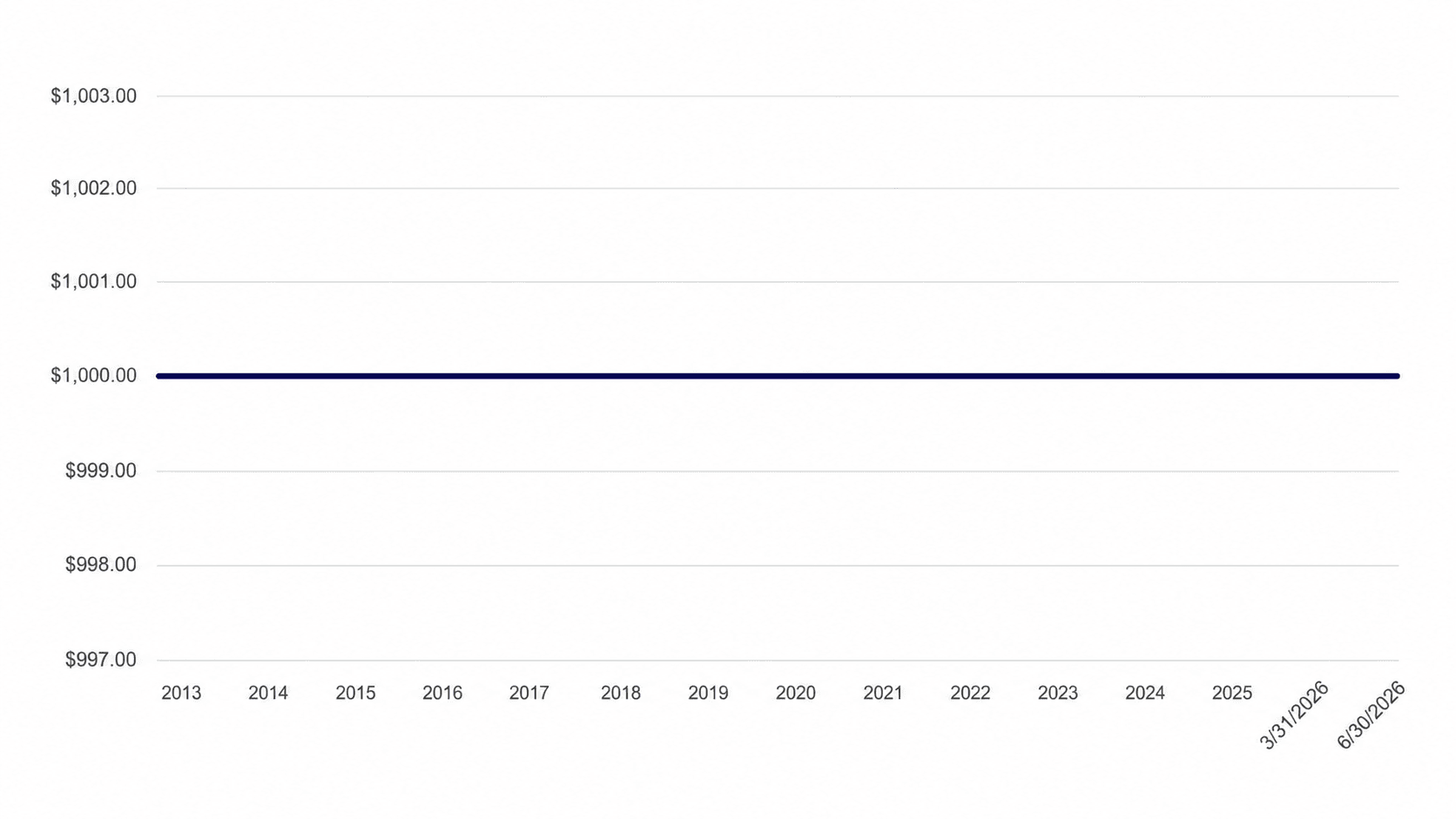

A key ingredient in the Income Fund’s success has been its stable net asset value (NAV). A stable NAV is important because it helps protect an investors’ principal investment. Since the Income Fund’s inception in 2013, the Income Fund has maintained a $1,000 NAV. The Income Fund continues to manage toward the goal of providing a balance of a stable NAV and target net annualized return between 6%-9%.

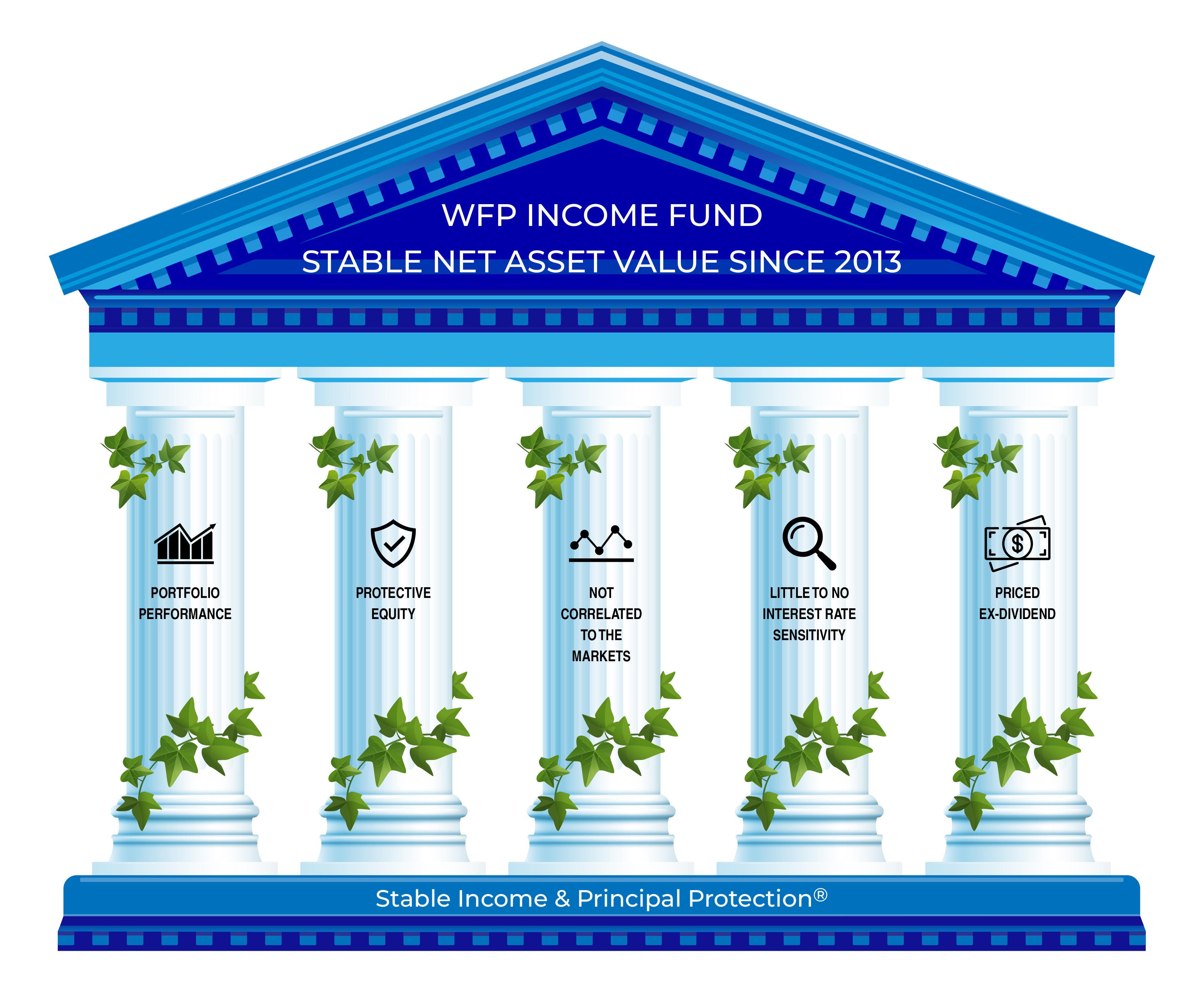

How Does the WFP Income Fund Achieve Stable NAV?

Achieving a stable NAV involves interplay of several key elements that deliver principal protection and consistent returns for investors, even when stock and bond markets fluctuate. Below are five factors that shape the Income Fund’s NAV.

Protective Equity Cushion

A protective equity cushion exists when the value of the real property exceeds the value of the loan. Specifically, the Income Fund’s loans are made at lower LTVs—often around 65%—resulting in the borrower having at-risk capital in the transaction (or “skin in the game”). That at-risk capital creates a buffer or cushion to help reduce the possibility of a default and reduce the potential loss exposure for the Income Fund should a default occur.

Wilshire’s experienced management team is committed to delivering stable portfolio performance through market cycles, driven by a combination of conservatively underwritten, shorter-term, loans made at lower loan-to-values (LTV), made at different stages of the market cycle, and which are diversified by asset type and geographic location.

The Income Fund is offered through a Private Placement and is not traded on any exchange. As a result, the Income Fund is not exposed to stock or bond market risk or volatility.

Fluctuating interest rates can impact the performance of stocks and bonds. However, the shorter-term loans in the Income Fund’s portfolio are held to maturity. As a result, unlike exchanged traded bonds and other fixed income investments which have an inverse relationship with interest rates, the Income Fund has little to no sensitivity to interest rate changes.

The Income Fund distributes cash flow to its investors once a month. New investments and redemptions occur after the dividends are distributed. By pricing the Income Fund ex-dividend, the Income Fund maintains a stable NAV and investors do not “buy the dividend.”

The Income Fund’s Advantage

Stable Income and Principal Protection®

Investors can enjoy consistent risk-adjusted returns and principal protection through the Income Fund’s strategy, underscored by the following attributes:

- Higher yields

- Monthly cash flow

- Stable net asset value

- Principal safeguards

- Well collateralized (low LTV) first lien position

- Established loan loss reserve

- Quantifiable protective equity cushion

- No correlation to the stock or bond markets

- Little to no sensitivity to interest rates

- Shorter duration (one year hard lock)

- Greater liquidity compared to non-traded REITs

- No load or commissions

- Secured by hard asset - real estate

- Diversification across sponsors, asset types, geographic location, and other factors

- Strong performance history

- Experienced management team

Loan Performance

PERFORMING LOANS

100%

REAL ESTATE OWNED

0%

NON-PERFORMING LOANS

0%

*as of March 31, 2024

Risk Mitigation

Because the Income Fund is designed with a balanced, conservative investment approach, we significantly reduce downside risk while delivering strong risk-adjusted returns for investors compared to other short-term fixed income investments.

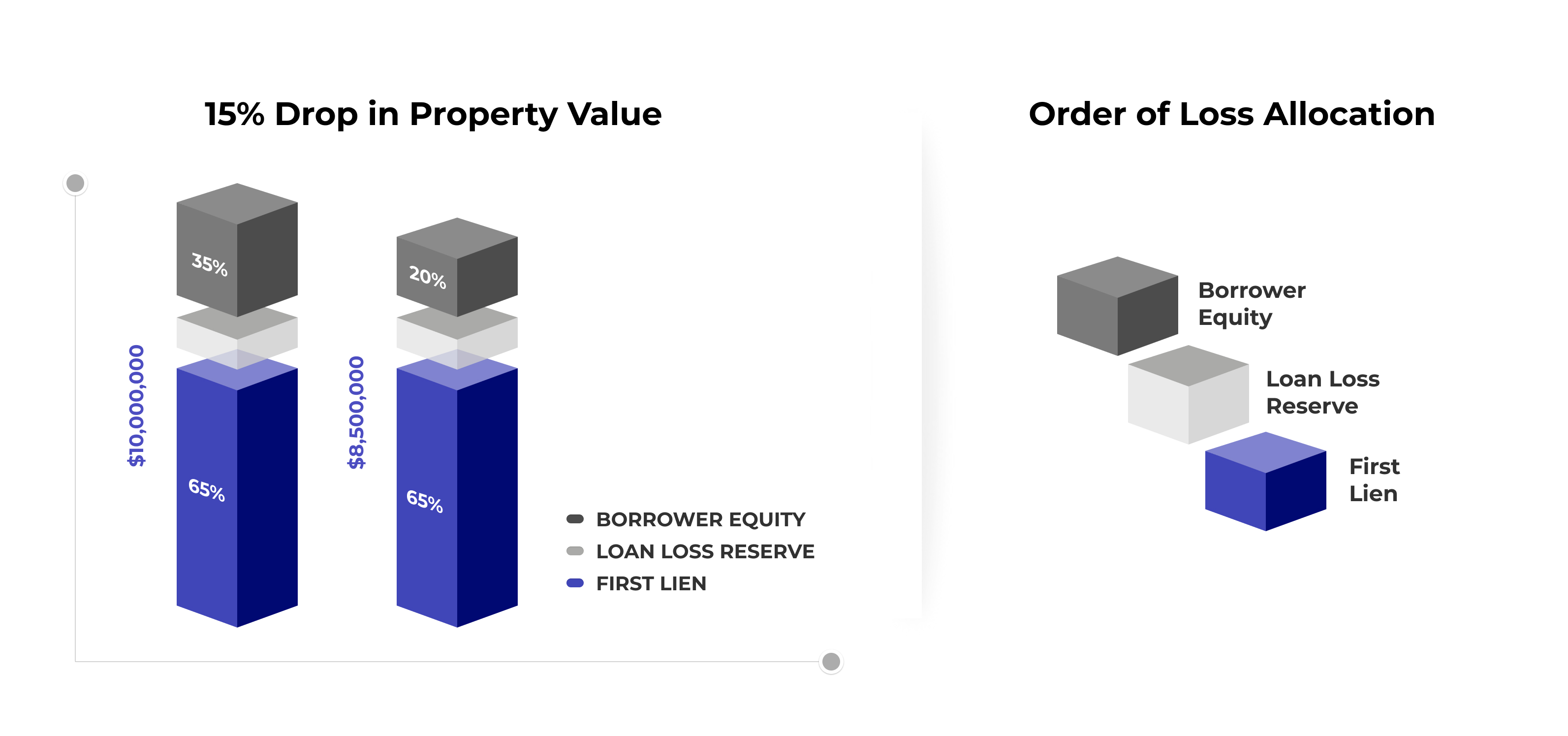

Loans secured by real estate as a first lien are in a priority position, making them an attractive option for investors seeking stable income and capital preservation. In addition to being in a first lien position, the loans in the Income Fund’s portfolio are made at a low weighted average LTV of approximately 65%. In the event of a borrower’s default, the Income Fund will be repaid before other debt and equity holders in the property.

Regarding Potential Risks

- Chances are remote that an investor would lose their entire investment. First, each member will have funds invested in a diversified portfolio of first mortgages and deeds of trust. For someone to lose their entire investment, many things would have to go wrong simultaneously. For example, all of the mortgages and deeds of trust within the portfolio would have to quickly go into default, the Fund would have to obtain all of its properties at foreclosure transactions without any third parties overbidding the Fund, and a situation would have to arise where there would not be a single buyer for any of the properties, regardless of price. The likelihood of all of these happening at once is practically impossible.

As is consistent with the nature of many investments, there is always the possibility of losing a portion of your invested principal. In the event that a loan within the Fund portfolio defaults, a foreclosure may occur. When that happens, there is a chance that the foreclosed property might sell for less than the amount of the loan, causing a loss. Such losses, however, should be minimal.

For example: The Fund makes a first loan of $3,250,000 to a borrower purchasing property for $5,000,000, which 65% of the property’s value (also known as a 65% loan-to-value or 65% LTV). Because of market or other conditions, the property value decreases and after default and foreclosure, the Fund sells the property for $3,100,000 (or a 38% reduction in the original purchase price), resulting in a $150,000 loss for the Fund. Assuming the Fund has $50,000,000 in portfolio investments and a member/investor has invested $100,000 (or 0.2% of the Fund), the investor’s pro rata share of the loss would be $300 (or $150,000 x 0.2%). However, if the Fund’s loan loss reserve is greater than $150,000, the loss would be absorbed by the reserve, and there would be no impact to the investor’s principal. If the Fund’s loan loss reserve is insufficient and the anticipated annualized return is 7%, the loss could be absorbed through a reduction in the return distributed to all investors in the fund by reducing the return from 7% to 6.7% (or $3,500,000 gross return - $150,000 loss = $3,350,000 adjusted return / $50,000,000) to mitigate or eliminate the impact of the loss to the investor’s principal investment. This example is for illustrative purposes only and if a loss occurs the actual results may vary.

In order to help mitigate the costs and potential losses in the Fund’s portfolio, the Fund may establish a loan loss reserve (“Loan Loss Reserve”) with a portion of the net proceeds of the capital contributions it receives or with cash from the Fund’s operations, or both. The Loss Reserve is designed to cover estimated losses from the Fund’s loans, investments, and operating activities. The methodology and amount of the Loss Reserve will be defined, adjusted, and managed by the Manager.

The combined benefit of the Fund’s Loan Loss Reserve and lower LTV ratio offers our investors downside risk protection and a buffer against potential losses. Because of the lower LTV ratios, a borrower who falls upon difficult times may have additional options because of their equity in the property (including the sale or refinance of the property) before a foreclosure is completed. In the event a property did go to auction as part of the foreclosure process, a third party could potentially overbid the Fund, leaving the Fund in the position to receive the principal investment back, in addition to interest and costs. Further, if the Fund obtains the property in foreclosure, it is possible the property could be sold for the amount owing under the loan or for a profit. Lastly, in the event of a loss on the property after a foreclosure and sale, the Loan Loss Reserve may be sufficient to absorb the loss, resulting in no impact to the investor’s principal.

Any money invested in real estate—whether it is debt or equity invested directly or through a limited partnership, REIT, or other structure—will be subject to some risk. Investments involving direct or indirect equity investments in real estate may have no buffer against changes in property values or other factors. To increase returns, investments may use debt or other leverage which is senior to the investor’s capital, have greater exposure to market and interest rate changes, and accept all the risks attendant to the management and operation of one or more properties. If, for example, there is a shortage in cash flow from the property underlying the investment and there is an inability to make the payments on the debt or pay insurance and property taxes, the senior lender in a leveraged investment vehicle can choose to foreclose the property causing investors to lose all or a portion of their principal investment.

On the other hand, the Fund’s portfolio consists of a diversified pool of first mortgages and deeds of trust secured by real estate. These are first priority liens and are senior to subordinate financing and the equity investors in the property. The Fund’s loans are made at lower loan-to-values, meaning that subordinate debt and the equity of the borrower in the property becomes a cushion or a buffer against loss for the Fund.

In addition, making and investing in loans in first lien position, the Fund will seek to diversify its loans and investments across borrowers and sponsors, property types, geographic location, and other factors to assist in mitigating risk. As compared to a real estate limited partnerships and other investments holding a single loan or investment (resulting in a concentration of risk) or multiple loans or investments with the same asset type, the same sponsors and/or the same structures (e.g. 100% single family loans), greater diversification will help to reduce portfolio risk. Because the Fund is targeting investments with shorter investment horizons, that may assist the Fund with managing variables impacting longer term investments, provide faster potential returns, and create greater potential liquidity.

Further, while exchange traded funds, partnerships, REITs and other real estate-backed securities will have a higher degree of liquidity, such investments are subject to greater volatility due to changes in interest rates or the markets in which they trade. Conversely, because the Fund is not exchange traded holds shorter-term loans and investments in its portfolio, the net asset value of the Fund is designed to remain stable and potentially less susceptible to the impacts of market and interest rate fluctuations.

As seasoned investors already know, the principal invested in stocks, bonds, and mutual funds may rise or fall, create gains or losses, due to a number of factors, including, the fundamentals of the underlying investments and fluctuations in respective markets in which those investments trade.

If “alternative investments” is defined as everything other than stocks, bonds and cash, the universe of alternative investments is very large, and the risk in each category of investment is varied, will differ in each potential investment in those categories, and may change based on a number of factors, including, changes in economic conditions, law and regulation, market conditions, and other factors. Therefore, a comprehensive discussion of risk of all alternative investments is beyond the scope of this discussion. A better approach for an investor may be to compare the risk of the Fund relative to other alternative investments in their portfolio and under consideration.

To assist with that comparison, investors may consider the following risk categories as a starting point:

- Market Risk. Market risk includes increases or decreases in an investment’s value due to volatility or fluctuation in the respective market in which those investments trade, and for real estate-based investments positive and negative impacts to the real estate market.

Exchange traded investments may have direct correlation to the stock and bond markets and/or interest rates, and some may be subject to volatility or fluctuation driven by factors completely unrelated to the fundamentals of the underlying investment or investment quality, such as investor sentiment, potential monetary action, geopolitical impacts, news, and other factors.

Because the Fund is not exchange traded and anticipates holding shorter-term loans and investments in its portfolio, the Fund is non-correlated to the stock and bond market and has little to no sensitivity to interest rate changes. Therefore, the Fund is potentially less susceptible to the impacts of stock and bond market volatility and interest rate fluctuations.

With respect to real estate market risk, the Fund’s portfolio will generally consist of loans in first lien position secured by real estate. Real estate values underlying these loans and investments are not immune from fluctuation or change. Real estate values have changed in the past and will change in the future.

What is unique about the Income Fund is the blend of risk mitigation strategies in place, as outlined below.

- Lower loan-to-value ratios provide a protective equity cushion to buffer against loss in the event of property value fluctuations or a borrower default.

- Shorter-term investments in real estate allows the Fund to react to real estate values and interest rates more quickly as compared to being locked into a 30-year mortgage. Additionally, the Fund has the opportunity to better gauge potential future market conditions over a 1- to 2-year time period as opposed to projecting market conditions 7 to 10 years into the future.

- Diversification across a number of segments, versus a pool of homogeneous loans, helps to mitigate the risk of an entire pool of loans and investments negatively reacting in a similar fashion at the same time. The Fund segments by geography, property types, borrowers, sponsors, maturities, rates, terms, and other mitigating factors.

- Interest Rate Risk. Interest rate risk is the potential for losses that result from a change in interest rates. For example, because of the inverse relationship between bond prices and interest rates, an increase in interest rates may result in a decrease in bond prices. Further, rising interest rates may negatively impact the capitalization rates used to value income producing real estate and the costs of operation.

Because the Fund invests in loans at lower loan-to-values with terms of approximately 1 to 3 years and holds those loans to maturity, the Fund is better able to react to changes in real estate values and interest rates as compared to being locked into 30-year mortgages.

- Liquidity Risk. Liquidity risk is the illiquidity or the inability to quickly or easily exist an investment or convert to cash. While exchange traded investments may have greater liquidity, the tradeoff is market risk and volatility.

Unlike other alternative investments that may have very long investment horizons (e.g. REITs with 7 to 10 year investment periods), the Fund allows investors to withdraw all or a portion of the investment after an initial 12-month period has passed. After that period, an investor may withdraw up to the lesser of 25% of your investment or $1,000,000 every consecutive 3 months. Additional restrictions on withdrawals may apply.

By having shorter-term loans with staggered maturities in the Fund’s portfolio, the Fund has internal liquidity as loans repay to help meet redemption requests.

- Regulatory Risk. Regulatory risk includes the risk that a change in laws or regulations will adversely affect a business, business sector, market or investment, or their respective prospects.

As an industry, real estate is subject to direct and indirect impacts of changing laws and regulations. During the COVID-19 pandemic, stay in place orders and prohibitions against gathering had both direct and indirect impact on certain real estate segments, such as hospitality and retail properties. Moratoriums on evictions and foreclosures impacted both owners and lenders in multifamily and other residential properties.

A certain level of regulatory risk is inevitable and an accepted part of real estate-based investments and, with certain exceptions, such as the emergency regulations described above, can be foreseen and managed. For example, laws and regulations related to leasing and tenant rights are an accepted part of the real estate business and can be managed.

Because of the nature of its operations, the Fund will be exposed to certain forms of regulatory risk and will seek to mitigate regulatory risk by managing existing requirements and foreseen changes where the regulatory risk is at an acceptable level for the applicable loan or investment. The Fund will avoid regulatory risk by not engaging in certain forms of investments where the risk is not in alignment with the Fund’s objectives or outweighs the potential rewards, such as entitlement risk associated with raw land, development, and ground-up construction loans and investments due to its risk with obtaining discretionary and non-discretionary approvals for matters like zoning, mapping, site plans, etc.

- Operational Risk. Operational risk includes the risk of loss resulting from inadequate or failed internal processes, procedures, people or systems.

In a real estate context, operational risk often relates to the plan and positioning of the property in the market and the owner or property manager’s execution of that plan.

Operational risk exists in most real estate investments, with some risk being greater than others. For example, ground up construction and later stabilization after completion has greater operational risk than the operational risk associated with a well-positioned, existing property managing tenant rollover. Further, there is greater operational risk in hotels and certain seniors housing properties compared to multifamily or warehouse properties.

Because the Fund will lend against and invest in various property types and properties in transition, operational risk will be present in various degrees in the loans and investments made by the Fund. The Fund will seek to mitigate those risks by lending to and investing with borrowers and sponsors who have experience and a successful track record in the specific asset class and circumstances giving rise to the lending and investment opportunities.

- Principal Risk. Principal risk involves the potential loss of the principal amount of an investment.

As addressed in this document, the Fund will seek to provide principal safeguards through the avoidance of certain risks, diversification in the Fund’s portfolio, shorter term lending and investment horizons, selection of borrowers and sponsors, the establishment of a Loan Loss Reserve, and underwriting the strength and viability of the plan of execution.

- Other Risks. Investors are encouraged to investigate and inquire about other potential risks in all investments they are contemplating, including the Fund. For more information about the potential risks of investing in the Fund, please review the Memorandum, including the section entitled “Risk Factors.”

- There are a number of potential actions that may be taken by the Manager and those actions will depend on the facts, nature, and circumstances of the default. Potential actions may include permitting additional cure periods, restructuring the loan, appointing a receiver to collect rents and manage the property, selling the loan, or foreclosing on the property. In the event that the Manager elects to sell the loan, likely buyers may include junior lien holders or other investors interested in owning the property. In an effort to protect and preserve the principal investment in the loan, the Manager has the ability to act quickly and aggressively in the event of default.

Declines in real estate values, longer marketing periods, lower absorption rates and other factors in a declining market may have an effect on the Fund’s portfolio. Specifically, if the value of the property which is collateral for a loan drops below the breakeven point for the loan, a loss would occur.

As an active market participant who has weathered several real estate cycles, the Manager’s principals have in-depth knowledge, expertise, and experience managing such risks. In anticipation of potential market changes, the current underwriting philosophy employed by the Manager results in the use of third-party valuations (e.g. appraisals), market analysis, stress testing of cash flows, capitalization rates and other factors, lower Loan-to-Value (LTV) ratios, shorter maturities, and other loan terms to help mitigate downside risk. When combined with the Loan Loss Reserve in the Fund, the result is a protective equity cushion for the loans within the Fund to help buffer the impact of changing real estate values and related market conditions.

Further, by keeping the terms of the loans short, the Fund has the ability to require existing borrowers to payoff or remargin (i.e. pay down the principal balance) their loans at maturity and to make new loans at the then current market values. This helps to reduce the risk of having a legacy portfolio of loans with longer maturities made at a time when property values were much higher.

While there are no assurances that the manager will be successful with all loans, in a waning market the Manager also has the ability to review and revise its underwriting approach and stress testing as necessary so that maximum Loan-to-Values (LTV), capitalization rates, loan maturities, and other loan terms are adjusted (i.e. may become more conservative) to address changing market conditions.

About Rewards

- The target annualized return for the Fund is 5.5% to 8%, net of Management fees and other Fund expenses. While we believe those returns are realistic, they are not guaranteed.

Yes, it is possible that future returns may be lower than returns paid in prior periods.

Once loans pay off, there is no guarantee that the Fund will find comparable quality loans at the same or a higher interest rate to replace them. Specifically, in order to stay competitive and maintain a portfolio of higher-quality loans, the Manager carefully monitors the market and adjusts interest rates as needed. Therefore, if market interest rates drop, the Manager may elect to lower the Fund’s interest rates on new loans to ensure that it receives a sufficient flow of new loan requests to meet the Fund’s portfolio needs. Conversely, if market interest rates rise, the Manager may elect to raise the Fund’s interest rates to capture additional yield for the Fund if loan quality may be maintained.

The Fund will also experience periods of time when committed capital is not fully invested in targeted real-estate-related loans and equity interests. Those periods will include the initial capital-raising and investment periods (“Ramp-Up Periods”), the periods during which capital is committed to fund loans and project-specific allocated capital prior to deployment of the capital, funds returned immediately following a loan payoff, and other similar events. At such times, the Fund will seek to employ such under-invested capital in short-term, interest-bearing investments to temporarily generate additional income for the Fund. However, overall returns in the Fund will be affected by the under-deployment of capital.

Other factors that may affect the Fund’s returns include potential increases or decreases in the Loan Loss Reserve (see above), or if a loan is not performing or is in foreclosure.

Over a longer period it is unlikely that the rate of return earned by the Fund’s members will be inferior to the rates offered by banks, credit unions, or other insured financial institutions on checking accounts, savings accounts, money market accounts, and certificates of deposit with a similar duction as the Fund (i.e. initial 12 month investment period). The explanation is relatively simple: the financial models of those institutions differ from the Fund.

Banks and other insured financial institutions have an incentive to reduce their cost of funds (a large portion of which is based on the rate they pay on deposits) to ensure a healthy Net Interest Margin (NIM). Essentially, the Net Interest Margin is the spread between a bank’s cost of funds and the rates they charge on loans. All other things being equal, the greater the NIM or spread, the more potential profit the bank receives. In a low interest rate environment like the one we have experienced over the last several years, the deposit rates offered by some banks may be under 1%. Therefore, while the banker may have the same objective of protecting their depositor’s principal, the banker’s incentive is to maximize returns for their shareholders and themselves and not necessarily their depositors.

However, the Fund, while not unlike a bank in many respects, has an incentive to maximize investor returns. A bank makes real estate loans using its depositor's money in essentially the same way the Fund makes loans with the money invested by its members. However, unlike depositors in a bank, Fund members receive all distributable cash earned by the Fund. The distributable cash in the Fund is primarily the interest received on the loan portfolio less the costs of operating the fund, working capital and loan loss reserves. As a result, the Fund has a targeted net annualized return to its investors of 6% to 8%.

- Generally, the distributions would be treated as ordinary income. However, investments through IRA, 401K, pension, and other qualified plans may receive more favorable tax treatment, such as the deferral of income taxes. We do not provide legal, tax, or accounting advice, and therefore, we recommend that you consult with your tax advisor about your particular tax situation.

Regarding Liquidity

- The operating agreement of the Fund allows you to withdraw all or a portion of the investment after an initial 12-month period has passed. After that period, you may withdraw up to the lesser of 25% of your investment or $1,000,000 every consecutive 3 months. Additional restrictions on withdrawals may apply. Earnings will accrue on your investment to the date of the withdrawal and there are no penalties for withdrawals.

There are several cash sources available for withdrawals, with the main source being loan payoffs. The Fund's portfolio consists of loans with different maturity dates, creating a laddering effect where loans payoff at different times creating liquidity in the Fund to pay withdrawal requests.

Another source is cash entering the Fund through new subscriptions. Effectively, cash from a new subscription to purchase Units in the Fund may be used to pay an outgoing member's request for a withdrawal.

Lastly, although it is not required to do so, underlying loans and investments may be sold to generate cash within the Fund.

Generally, less than 1 month. Once the Subscription Documents are completed by the investor and investment funds are deposited into the Fund’s subscription account, the Manager must promptly accept or reject the Subscription Documents. If the Subscription Documents are rejected, the investor’s funds will be promptly refunded to that investor from the subscription account. If the Subscription Documents are accepted, the investor’s funds will be moved into the Fund’s general account on the first day of the month following the acceptance of the subscription and the investor will become a member of the Fund on that date.

Subject to the Subscription Documents being accepted by the Manager, an investor’s funds may be borrowed from the Subscription Account at a rate of 4% per annum prior to the investor being admitted as a member of the Fund on the first day of the following month. Therefore, depending on when an investor invests with the fund (i.e. early in the month or later in the month), if accepted by the Manager, funds may be held in the subscription account from a few days to a few weeks, but less than 1 month.

Fund Borrowers

- Many of the Fund's borrowers are professional real estate investors and/or owners and operators of commercial and residential real estate. As such, they need an efficient lending source when capitalizing on market opportunities—and they are willing to pay a premium in the interest rate and fees on the loan in exchange for speed and efficiency. It becomes a business expense of the transaction. Therefore, because the Manager and the Fund have a funding platform that can deliver the speed and efficiency desired by those borrowers, they can command higher interest rates and fees than banks and other institutional lenders. This results in higher yielding loans in the Fund’s portfolio and higher risk-adjusted returns for the Fund’s investors.

Miscellaneous

The Fund has engaged the services of Armanino, LLP (“Armanino”) to perform an annual audit. Further, Armanino assists with a review of the Fund’s monthly reconciliations and member distributions.

Armanino is one of the largest California based Certified Public Accounting firms and one of the top 25 accounting firms in the United States. They have been providing accounting and consulting services for over 50 years. Armanino provides services to more California mortgage pools and funds than any other firm in the state and are rapidly becoming a national leader in this industry. Armanino is subject to review by the Public Company Accounting Oversight Board (“PCAOB”), a private-sector, nonprofit corporation created by the Sarbanes–Oxley Act of 2002 to oversee the audits of public companies and other issuers in order to protect the interests of investors and further the public interest in the preparation of informative, accurate, and independent audit reports. Further, Armanino is a member of Moore Global (formerly, Moore Stephens), one of the world’s major accounting and consulting networks and provides access to over 260 independent accounting firms in 110 countries.

- As described above, the Fund "bridges" the gap in timing or financing borrowers often experience when they need speed and efficiency to capitalize on a market opportunity, or before they can position their property for more traditional institutional financing or a sale.

Shorter and medium term loans allow the Fund to manage its portfolio in several important ways. By keeping the terms of the loans short, the Fund has the ability to require existing borrowers to pay off or remargin (i.e. pay down the principal balance) their loans at maturity. This helps to reduce the risk of having a legacy portfolio of loans with longer maturities made at a time when property values were much higher. In addition, as loans pay off, the Fund can make new loans at the then current market values. This helps to preserve the protective equity cushion in the Fund.

Shorter and medium term loans also give the Fund the opportunity to react to a changing interest rate environment. If interest rates increase as loans pay off, the Fund may reinvest that capital in loans with higher interest rates resulting in higher relative yields for the Fund’s members.

In a waning market, as opposed to being locked into the terms and conditions on longer term loans, the Manager has the ability to review and revise its underwriting approach and stress testing as necessary to adjust to changing market conditions and mitigate overall portfolio risk as new loans are made.

Lastly, shorter and medium term loans create liquidity in the Fund’s portfolio to address withdrawal requests by the Fund’s members.

- Investment Type: The Fund is a professionally managed fund investing in short term loans secured by first trust deeds and mortgages against real estate throughout the United States. It should be measured against other conservative, short-term, fixed income investments in your portfolio.

- Investment Objective: Stable Income & Principal Protection®. The Fund strives to provide a combination of consistent risk-adjusted returns and principal protection through diversification and the protective equity cushion in the loan portfolio.

- Investment Strategy Justification: The Fund is a short-term, fixed income investment alternative that provides the following attributes and benefits:

-

- Higher Yields

-

- Monthly Distributions

-

- Stable Net Asset Value

-

- Principal Safeguards

-

- Well Collateralized (Low LTV) Portfolio of Loans in First Lien Position

-

- Established Loan Loss Reserve

-

- Quantifiable Protective Equity Cushion

-

- No Correlation to Stock or Bond Markets

-

- Little-To-No Sensitivity to Interest Rates

-

- Short Term with a One Year Hard Lock

-

- Greater Liquidity Compared to Non-Traded REITS and Other Alternative Investments

-

- No Load or Commissions

-

- Secured by Hard Asset - Real Estate

-

- Diversification Across Sponsors, Asset Types, Geographic Location and Other Factors

-

- Strong Performance History

-

- Experienced Management Team

Subscribe to Our Newsletter

Notice

THE INFORMATION IN THESE FREQUENTLY ASKED QUESTIONS IS DESIGNED AS A GUIDE FOR PROSPECTIVE INVESTORS TO ASSIST IN FOLLOWING THE FORMAL PRESENTATION OF INFORMATION CONTAINED IN THE SECOND AMENDED AND RESTATED PRIVATE PLACEMENT MEMORANDUM OF THE WFP INCOME FUND, LLC DATED JANUARY 1, 2022 (INCLUSIVE OF EXHIBITS THERETO AND ANY SUPPLEMENTS, THE “MEMORANDUM”), WHICH PROVIDES A DESCRIPTION OF THE FUND, THE TERMS OF ITS PRIVATE PLACEMENT, A DISCUSSION OF RISK FACTORS, A COPY OF THE FUND’S SECOND AMENDED AND RESTATED LIMITED LIABILITY COMPANY OPERATING AGREEMENT, A SUBSCRIPTION AGREEMENT AND OTHER INFORMATION RELATED TO THE FUND. THE INFORMATION CONTAINED IN THESE FREQUENTLY ASKED QUESTIONS IS NOT AN OFFER TO SELL OR THE SOLICITATION OF OFFERS TO PURCHASE THE SECURITIES OF THE FUND OR OTHERWISE. INVESTMENTS MAY ONLY BE SOLD TO ACCREDITED INVESTORS WHO RECEIVE THE MEMORANDUM. DISTRIBUTION OF THESE FREQUENTLY ASKED QUESTIONS TO PROSPECTIVE INVESTORS IS NOT AUTHORIZED UNLESS ACCOMPANIED BY THE MEMORANDUM. IN THE EVENT OF ANY CONFLICT BETWEEN THE INFORMATION CONTAINED IN THESE FREQUENTLY ASKED QUESTIONS AND THE MEMORANDUM, THE MEMORANDUM SHALL CONTROL. SEE ALSO ADDITIONAL DISCLOSURES BELOW AND RISK FACTORS IN THE MEMORANDUM.

Further Questions

If you have further questions, please contact Donald Pelgrim, Chief Executive Officer of Wilshire Finance Partners, at (866) 575-5070.

ADDITIONAL DISCLOSURES

Wilshire Finance Partners, Inc. specializes in real estate finance and investments and is the manager of the WFP Income Fund, LLC (the “Fund”). This communication is not an offer to sell or the solicitation of offers to purchase the securities of the Fund or otherwise. The purpose of this communication is to provide an overview of the Fund and its private placement. Persons interested in learning about the Fund and its private placement will be provided with the Fund’s Second Amended and Restated Private Placement Memorandum, dated January 1, 2022 (inclusive of exhibits thereto and any supplements, the “Memorandum”), which provides a description of the Fund, the terms of its private placement, a discussion of risk factors, a copy of the Fund’s Second Amended and Restated Limited Liability Company Operating Agreement, a Subscription Agreement and other information related to the Fund. This communication contains certain forward-looking statements regarding the Fund’s investment objectives and strategies. The forward-looking statements are based on current expectations that involve numerous risks and uncertainties which are difficult or impossible to predict accurately and many of which are beyond the control of Wilshire Finance Partners, as the manager of the Fund. Although Wilshire Finance Partners believes that the assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate and, therefore, there can be no assurance that the forward-looking statements will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements, the inclusion of such information should not be regarded as a representation by Wilshire Finance Partners, any placement agent, or any other person, that the objectives and strategies of the Fund will be achieved. An investment in the Fund may be made solely by accredited investors (which for natural persons, are investors who meet certain minimum annual income or net worth threshold), who are provided with the Memorandum and who complete, execute and deliver the subscription documents included therein. The Fund’s securities are being offered in reliance on an exemption from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”) and are not required to comply with specific disclosure requirements that apply to registration under the Securities Act. The Securities Exchange Commission has not passed upon the merits of or given its approval to the securities, the terms of the offering, or the accuracy or completeness of any offering materials. The securities are subject to legal restrictions on transfer and resale and investors should not assume they will be able to resell the securities. Past performance is not indicative of future results. Investing in the Fund involves substantial risk, including loss of investment, and is not suitable for all investors.

In the event of any conflict between the information in these Frequently Asked Questions and the Memorandum, the Memorandum will control.

Wilshire Finance Partners, Inc. is licensed by the California Department of Real Estate, Broker License number 01523207 and California Department of Financial Protection and Innovation, Finance Lenders License number 603K729. The WFP Income Fund, LLC is licensed by the California Department of Financial Protection and Innovation, Finance Lenders License number 603K726, the WFP Income Fund REIT, LLC is licensed by the California Department of Financial Protection and Innovation, Finance Lenders License number 60DBO-99184, and the WFP Opportunity Fund, LLC is licensed by the California Department of Financial Protection and Innovation, Finance Lenders License number 603K725.